Subscribe now to get notified about IU Jharkhand journal updates!

Impact Of Ethical Business Practices On Organisational Competitiveness A Study On Service Sector In India

Abstract :

Ethics concern an individual's moral judgments about right and wrong. It seems like the larger a corporation gets, the slimier their actions become. Many a times business houses got involved in unethical business practices to increase their profits or to improve their capability in market. Indian Service Sector, which is the youngest and fastest growing sector of economy, is the foremost tool of growth and development of nation. More empirical and theoretical research work is needed in the sphere, to firm up the exact modular relationship between the societal culture and business ethics. Hypothesis tested are about the degree of Indian Service Corporates' recognition of the existence of ethics in today’s competitive business environment and about the degree of relationship between organisational and business growth and ethical business practices in India. Being a Qualitative Research, design opted for this research will be Descriptive Research Design, where Survey will be the Primary Method of Data Collection. In some cases, Observation will be used as a supplementary source of data collection whenever applicable. Companies in service sector in India will be considered as population. A sample of 200 Service Concerns PAN India is taken into consideration. An additional study will be conducted from the general public, with a sample of 60 Respondents Each from the Three Corporate Metropolitan Regions of Bangalore - Hyderabad - Chennai, Delhi NCR, Mumbai - Pune - Ahmedabad. Structured Equation Modeling & Path Analysis as well as Chi-Square Automatic Interaction Detection (CHAID) Technique is proposed to be used for the purpose of analysis.

Keywords :

Ethical Business Practices, Service Sector in India, Service Delivery Ethics, Methodology for Ethical Research, Study LimitationsINTRODUCTION

Ethics concern an individual's moral judgments about right and wrong. Decisions taken within an organization may be made by individuals or groups, but whoever makes them will be influenced by the culture of the company. The decision to behave ethically is a moral one; employees must decide what they think is the right course of action. This may involve rejecting the route that would lead to the biggest short-term profit. Unethical behaviour or a lack of corporate social responsibility, by comparison, may damage a firm's reputation and make it less appealing to stakeholders. Profits could fall as a result. It seems like the larger a corporation gets, the slimier their actions become. When big profits are a company’s largest — and only — concern, their employees and the world in general tends to suffer. Here are companies that have engaged in terribly unethical business practices and are, fortunately, being called out for it.

One of the most important aspects of any car company is safety — the concern for safety, how both employees and consumers are kept safe, and how issues are handled should a safety concern arise. Toyota made a huge and unethical failure in 2010 when they basically betrayed their promise as a company by ignoring safety concerns and delaying recall investigations just so they could save a little money. After confronted with safety concerns regarding faulty brakes and sticking pedals in 2009, Toyota said that phasing in side airbags saved $124 million and 50,000, the cost of what it would have taken to recall and fix vehicles. They also stated that delaying a rule for tougher door locks saved them $11 million.

Infamous Halliburton is one of the world’s largest oil corporations worldwide, operating in over 80 countries. They are also debatably one of the most evil companies in the entire world. Halliburton’s unethical offenses are so many that they are best summarized in list form:

- Halliburton has been accused, multiple times, of engaging in business transactions with countries with which trades are prohibited by the US government.

- Halliburton has been accused of overbilling the US army for food and oil supplies during the Iraq war, 2003.

- Halliburton has been accused of covering up violations of corruption laws and misleading investigators by a former Halliburton employee who states that he received criminal notes on how to handle federal investigations in an email intended for another employee.

- Other ex-Halliburton employees accuse Halliburton of mismanaging waste in Iraq, citing a particular instance in which they abandoned an $85,000 due to a flat tire and charged approximately $100 for fifteen pounds of laundering services.

- A female employee sued Halliburton, claiming that she was gang-raped by fellow employees in Iraq.

- Halliburton faces multiple additional lawsuits for endangering employees, endangering National Guard members by unknowingly exposing them to hazardous chemicals, and over oil spills said to be the result of careless and unsafe practices.

Everyone wants an iPhone and no one really cares if it were made by tiny child slaves who are forced to work in dangerous conditions, inhaling cancerous vapors, for 10 hours a day, seven days a week. And that is why Apple continues to be so profitable. But as beautiful as their products are, the production side of their business is a dark, horrific and unethical one. Apple manufacturer Foxconn is like hell on earth. Conditions at this plant are so miserable that “anti-suicide nets” had to be installed beneath the windows after a whopping 17 employees leapt to their deaths in protests of the horrific things they had to endure on a daily basis. Living quarters like tiny college dorms in a gigantic beehive type factory, each crammed with crappy bunk beds. Exhausting hours, humiliating discipline, unreasonable workloads, and pressure to reduce overtime resulting in lower paychecks are just some of the crappy conditions faced by thousands of Foxconn employees on a daily basis.

The controversy began in 2006 and is still happening today. And while Apple has made efforts to branch out and use some different manufacturers to produce their products, unethical Foxconn is still their go-to company. Besides using Foxconn, Apple co-founder Steve Wozniak claimed that Apple was engaging in unethical tax practices by utilizing an Irish tax loophole to avoid paying billions in taxes on international sales.

All these reveals us that many a times business houses got involved in unethical business practices to increase their profits or to improve their capability in market. Such practices did throughout the world. This urges out the need for studying out the matter. Approaching towards our Focus Group, i.e., Indian Service Sector, which is the youngest and also the fastest growing sector of Economy & having the largest share in the structure & growth of the economy, is the foremost tool of growth and development of nation, we can have. but this sector in recent past many a times, especially in India, has been accused of its service failures and incompetence, arising out of irresponsible behavior / treatise of management or professionals at various levels. Now in this research focusing on Indian Service Sector Corporates, we will study the status of ethics in their practices and the need and possibility of revival there. The objectives and scope of this study are as follows:

1.1 Objectives of the Study

To make a study conducive and relevant it is necessary to formulate objectives of the study to make it relevant for the researcher to design and conduct a systematic schema for the purpose of research. Likewise, the objectives of this research are:

- To identify the ethical practices followed by Indian Service Corporates; and

- To find the Impact of Ethical Business Practices on the Competitiveness of Service Sector in India.

1.2 Scope of the Study

This research regarding the Existence and Practicability of Ethical Conduct in the Present Competitive Business Environment is prepared for the period starting from the date of project inception to the project conclusion (as required for the adequate analysis of the phenomena). So this project presents an overview regarding the Indian business practices in service sector for this period and other allied facts and figures. Apart from that this report also gives us a brief view of the global trend and the situation of the Indian economy in the present competitive scenario

1.3 Hypothesis to be tested

Hypothesis 1

Ho1: 0= MEAN e: Indian Service Corporates don’t recognize the existence of ethics in today’s competitive business environment.

Ha1A: 0 < MEAN e: Indian Service Corporates recognize the existence of ethics even in today’s competitive business environment.

Ha1B: 0.05 ≤ MEAN e: Indian Service Corporates considerably recognize the existence of ethics even in today’s competitive business environment.

Ha1C: 0.75 ≤ MEAN e: Indian Service Corporates strongly recognize the existence of ethics even in today’s competitive business environment.

Ha1D: 1 = MEAN e: Indian Service Corporates in wholly recognize the existence of ethics even in today’s competitive business environment.

Hypothesis 2

Ho2A: SD g ≠ SD e: there is no / an imperfect relation in between organizational and business growth and ethical services delivery management practices in India.

Ho2B: SD g< SD e: there is no / a lesser influencing relationship between organizational and business growth and ethical services delivery management practices in India.

Ha2A: SD g = SD e: there is a perfect / directly influencing relationship between organizational and business growth and ethical services delivery management practices in India.

Ha2B: SD g ≥ SD e: there is an exponential & directly influencing relationship between organizational and business growth and ethical services delivery management practices in India.

Review Of Literature

The Greeks and Romans defined Ethos as the compilation of the usages, ideas, standards, and codes by which a group lives’. Ethics pertained to the ethos – and therefore were the standard of right. The term "business ethics" is used in a lot of different ways. Business ethics is a form of applied ethics (Broni, 2010) that examines ethical principles and moral or ethical problems that arise in a business environment (Solomon, 1991). It applies to all aspects of business conduct (Baumhart, 1968; Ferell & Fraedrich, 1997; Singer, 1991) and is relevant to the conduct of individuals and business organizations as a whole (Bernard, 1972; Donaldson, 1982).

Applied ethics is a field of ethics that deals with ethical questions in many fields such as technical, legal, business and medical ethics (Preston, 1997). Business ethics consists of a set of moral principles and values (Jones, Parker & Bos, 2005:17) that govern the behaviour of the organization with respect to what is right and what is wrong (Badiou, 2001; Seglin, 2003). It spells out the basic philosophy and priorities of an organization in concrete terms (French, 1979; French, 1995). It also contains the prohibitions at the workplace (Collier & Esteban 2007; Duska, 1999). It provides a framework on which the organization could be legally governed. With time, certain moral philosophies have helped in the evolution of four basic concepts of ethics. They are deontologism, relativism, egoism, and utilitarianism (Kotsiris, 2003). This research will try to sheds light on the practical existence of basic principles of business ethics and these aforesaid concepts.

Business ethics is the behaviour that a business adheres to in its daily dealings with the world (Borgerson & Schroeder, 2008). The ethics of a particular business can be diverse (Solomon, 1983). They apply not only to how the business interacts with the world at large, but also to their one-on-one dealings with a single customer (Solomon, 1991). Many businesses have gained a bad reputation just by being in business (Carr, 1968). To some people, businesses are interested in making money, and that is the bottom line (Solomon, 1983). It could be called capitalism in its purest form (Antoniou, 2008).

Making money is not wrong in itself. It is the manner in which some businesses conduct themselves that brings up the question of ethical behaviour (Maitland, 1994). Good business ethics (American Psychological Association, 1992, 1999, 2001) should be a part of every business (Preuss, 1997). There are many factors to consider (Michalos, 1995). When a company does business with another that is considered unethical, does this make the first company unethical by association (Kahneman - Knetsch & Thaler, 1986; Velasquez, 1983)? Some people would say yes, the first business has a responsibility (Michalos, 1995)and it is now a link in the chain of unethical businesses (Κanungο & Mendoca, 1996). Many global businesses, including most of the major brands that the public use, can be seen not to think too highly of good business ethics (Maitland, 1994). Many major brands have been fined millions for breaking ethical business laws (Cory, 2005).

Money is the major deciding factor (Seglin, 2003). If a company does not adhere to business ethics and breaks the laws, they usually end up being fined (Drucker, 1981). Many companies broken anti-trust, ethical and environmental laws and received fines worth millions (Velasquez, 1983). The problem is that the amount of money these companies are making outweighs the fines applied (Green, 1991). The profits blind the companies to their lack of business ethics, and the money sign wins (DeGeorge, 1999). A business may be a multi-million seller, but does it use good business ethics and do people care (French, 1979)? There are popular soft drinks, fast food restaurants, and petroleum agencies that have been fined time and time again for unethical behaviour (Harwood, 1996). Business ethics should eliminate exploitation, from the sweat shop children who are making sneakers to the coffee serving staff that is being ripped off in wages. Business ethics can be applied to everything from the trees cut down to make the paper that a business sells to the ramifications of importing coffee from certain countries (Aiken, 1991).In the end, it may be up to the public to make sure that a company adheres to correct business ethics (Clarke, 2004). If the company is making large amounts of money, they may not wish to pay too close attention to their ethical behaviour (Behrman, 1988).

There are many companies that pride themselves in their correct business ethics (Stark, 1993), but in this competitive world, they are becoming very few and far between (Knight, 1980). In the increasingly conscience-focused marketplaces of the 21st century, the demand for more ethical business processes and actions (known as ethicism) is increasing (Donaldson, 1982). Simultaneously, pressure is applied on industry to improve business ethics through new public initiatives and laws (e.g. higher luxury taxes). Businesses can often attain short-term gains by acting in an unethical fashion (Sunstein, 2002). however, such behaviours tend to undermine the economy over time (Velasquez, 1983).

Business ethics can be both a normative and a descriptive discipline (Abram's, 1954). As a corporate practice and a career specialization, the field is primarily normative. In academia descriptive approaches are also taken. The range and quantity of business ethical issues reflects the degree to which business is perceived to be at odds with non-economic social values. Historically, interest in business ethics accelerated dramatically during the 1980s and 1990s, both within major corporations and within academia (Cory, 2005). For example, today, most of the major corporates, on their websites, lay emphasis on commitment to promoting non-economic social values under a variety of headings. Corporations have redefined their core values, in some cases, in the light of business ethical considerations.

Business management scholars have been searching for a business case for CSR since the origins of the concept in the 1960s.The CSR of the 1960s and 1970s was motivated by social considerations, not economic ones. The socially responsible investment movement establishing a positive relationship between corporate social performance (CSP) and corporate financial performance (CFP) has been a long-standing pursuit of researchers. This endeavour has been described as a “30-year quest for an empirical relationship between a corporation’s social initiatives and its financial performance.”Only in the past 20 to 25 years, the concept of business ethics consulting has developed, originally provided on an ad hoc basis by academics that were doing research into business ethics, but since the 1990s there has been an increase in the number of firms that provide formal ethics consulting services. In the recent decade, many authors and researchers has given their opinion on the subject. Some eminent ones of these are as follows:

Campbell and Malan (2002) suggests that Ethical business is good business, especially if you want to stay in business. "Recent corporate collapses, as a result of poor corporate governance, both locally and internationally, have once again emphasized the importance of doing business ethically,""Good ethics makes good business sense," stresses Malan. "Long-term profitability depends on sustainability, and to ensure sustainability in the twenty-first century you need to focus on integrated financial, ethical and environmental performance at the same time – the so-called 'triple bottom line'," he argues. he further adds that 'basic ethical infrastructure' involves such things as official company codes of conduct and ethics and official company confidential reporting lines to allow 'whistle-blowers' to report wrongdoing.

"Codes of ethics are often not supported by training in ethical practices for employees, it is not clear whether confidential reporting lines are used effectively and, in many cases, no senior manager is clearly designated to handle ethics issues," he reports."Companies need to refocus on the ethics function and ensure that their basic infrastructure is backed up by effective ethics management practices," he states. He supported his opinion by second King Report on Corporate Governance, which clearly states that companies should demonstrate a commitment to organizational integrity.

Blowfield (2003) in his research embellishes that we need a more rigorous approach to understanding whose rights are being considered and whose are being denied. There is evidence that certain issues will be overlooked or excluded from standards in the future because they cannot be codified or measured. What is more, others have de facto been removed from negotiation as a condition of business participation in ethical sourcing. Put another way, businesses’ expectations regarding their engagement may be that civil society and government will leave unquestioned such rights as the freedom to trade, to invest and disinvest and to defer to market mechanisms as the arbiter of fair price.

In particular, once one gets beyond the broadest definitions, sustainability needs to be recognized as a contested and subjective concept, the negotiation of which will be influenced by the perceptions and, above all, power of different parties. A just outcome from such negotiation (and justice is an inherent part of sustainability) is not simply a question of attempting to involve interested parties (although, given the differences in interests, education, location, culture, etc., that in itself will be an immense challenge) but also a question of developing means of negotiation that are not inherently biased towards a particular party or world-view. This may seem to support the notion of stakeholder engagement or partnership as essential to sustainable supply chain management, building on the widespread advocacy of such approaches in corporate social responsibility literature. Yet these notions may be as ideationally rooted as the other instruments of ethical sourcing, leading to the possibility that they will only recognize, benefit and reproduce those who conform to the social, economic and political formations from which such instruments have emerged. And if this comment serves as a note of caution for civil-society organizations eager to embrace multi-sectoral partnerships it should also serve the same purpose for those keen to promote a business case for ethical sourcing—business will be unable to limit risks, enhance its reputation or simply obtain a reliable supply of commodities for the future if it employs approaches that ignore or misrepresent the well-being of those in developing countries.

Mulla (2003) comments upon that the efficacy of corporate initiatives in the ethical regard in Indian Environment remains to be seen. Till then Employees' personal initiative and dynamic leadership for a sustainable moral ethical character will work for.

Dunning and Wales (2004) while giving their opinion on Global Capitalism says that If global capitalism, arguably the most efficient wealth creating system currently known to man, is to be both economically viable and socially acceptable, each of its four constituent institutions (markets, governments, supranational agencies, and civil society) must not only be technically competent, but also be buttressed and challenged by a strong moral ethos.

Labbai (2007), further extending the approach, argues that companies must adopt and disseminate a written Code of Ethics, build a company tradition of ethical behaviour, and hold its people fully responsible for observing ethical and legal guidelines. He acclaims that companies, who are able to innovate new solutions and values in a socially responsible way, are most likely to succeed.

Seshadri, Raghawan and Hedge (2007) expresses their view that business ethics are also about creating an ethically sound working environment within organization and about modelling ethical behaviour by leadership. Their research suggests that it makes good long term business sense to be ethical.

Freeman, York and Stewart (2008) exclaims that Human life is rich and complex and not reducible solely to an economic calculation. If we have learned anything from the collapse of state socialism, it is that governments and centralized approaches do not work very well. Businesses can and often do stand for something more than profitability. Some, like IBM, stand for creating value for customers, employees, and shareholders. On this behalf, they had defined a few of Green principles at large towards the stakeholders.

Pivato, Misani and Tencati (2008) illustrate the role of trust as a mediating variable which shapes the relationship between CSR activities and firm performance. Barnett (2007)set out the construct of stakeholder influence capacity, which illustrates how situational contingencies may affect the impact of CSR activities on firm financial performance. It is critical to apply the contingency perspective as suggested by Barnett (2007) and account for the role of mediating variables as proposed by Pivato (2008) in the exploration of the relationship between CSR and firm financial performance.

Pal (2009) further expands the view stating that through the positive linkage between directors' remuneration & revenue from additionality, the ethical arm of corporate governance would further be strengthened.

Carroll and Shabana (2010) exemplifies that the broad view of the business case for CSR enables the firm to enhance its competitive advantage and create win–win relationships with its stakeholders, in addition to realizing gains from cost and risk reduction and legitimacy and reputation benefits, which are realized through the narrow view. The broad view enhances the acceptance of the business case for CSR, because it acknowledges the complex and interrelated nature of the relationship between CSR and firm financial performance. Recognizing this complexity translates into a clearer understanding of the impact of CSR initiatives on firm financial performance while accounting for the effects of mediating variables and situational contingencies. To formulate a successful CSR strategy, firms must understand that the benefits of CSR are dependent on mediating variables and situational contingencies.

Velentzas and Broni (2010) expresses that nowadays ethics in business are obligated because many businessmen are only interested in making money despite the ethical costs or the harm they would probably cause to people or even to nature (environmental pollution). As per them, many organizations are choosing to make a public commitment to ethical business by formulating codes of conduct and operating principles. In doing so, they must translate into action the concepts of personal and corporate accountability, corporate giving and corporate governance.

Jalil, Azam and Rahman (2010) bring out a more comprehensive perspective. As per them, ethics and ethical behaviour are issues which are increasingly being focused on the business community today. People are becoming more concerned about what is actually happening in business organizations in the name of competition, growth, and profitability. Organizations are crossing the red zone of ethics and ethical behaviours. A growing number of organizations are constantly surveying and evaluating the unethical practice in business organizations worldwide. It is empirically proved that ethical practices in business organizations help to create favorable relationships with other organizations and can also establish long-term positive relationships with existing and potential future customers. As per their research, it is very essential to have a code of business ethics in every business organization and this code of business ethics must be implemented in the organization in objective and effective way.

Smart, Barman and Gunasekera (2010) observes that strong ethical policies that go beyond upholding the law can add great value to a brand, whereas a failure to do the right thing can cause social, economic and environmental damage, undermining a company’s long-term prospects in the process. They recommends that Corporate communications and reporting on sustainability need to do more than just pay lip service to the green agenda, and hence, ethics must be embedded in business models, organizational strategy and decision making processes. Governance structures should include people with appropriate skills to scrutinize performance and strategy across social, ethical and environmental issues.

Mishra and Sharma (2010) Extending the aspect disserts that an Effective CSR Policy within specific industries and companies is becoming increasingly accepted, but its implementation varies all across.

Tonello (2011) interprets that in the last decade; in particular, empirical research has brought evidence of the measurable payoff of corporate social responsibility (CSR) initiatives to companies as well as their stakeholders. Companies have a variety of reasons for being attentive to CSR. It had to do with the long-standing divide between those who, like the late economist Milton Friedman, believed that the corporation should pursue only its shareholders’ economic interests and those who conceive the business organization as a nexus of relations involving a variety of stakeholders (employees, suppliers, customers, and the community where the company operates) without which durable shareholder value creation is impossible.

He asserts Another impetus that Even though CSR came about because of concerns about businesses’ detrimental impacts on society, the theme of making money by improving society has also always been in the minds of early thinkers and practitioners: with the passage of time and the increase in resources being dedicated to CSR pursuits, it was only natural that questions would begin to be raised about whether CSR was making economic sense. He recognizes that In addition to the guardians of companies’ financial well-being, other groups such as Shareholders, Social activists, Governmental bodies, Consumers, are well concerned with the wellness of entity in the pursuit of their respective combined interest. Considering such counterparts, positive effects of CSR on firm performance includes Reducing Costs and Risks, Equal employment opportunity policies and practices, Energy-saving and other environmentally sound production practices, Community relations management, Gaining Competitive Advantage, Developing Reputation and Legitimacy, Seeking Win-Win Outcomes through Synergistic Value Creation.

James (2013) acclaims that business organizations that contribute to the increase in the density of local food production, they identify the emerging business practices, ethics principles, and competition in this regard and new cooperatives will be better aware of viable business models based on ethics. Donaldson describes that Business ethics are business actions in light of some aspect of human value. There is no viable universal standard that can be applied to everyone. This separates them from what would have been the ethos or mores of the people today.

Nainawat and Meena (2013) address ethics as the first line of defense against corruption and stresses that the absence of Good Corporate Governance will definitely lead to the questionable practices and corporate failures.

Rebelly and Ragidi (2014), in their study based upon NTPC, asserts that Companies must make profit to survive with growth, but within the ethical bounds.

Husssaini (2014), in her research on Top Indian IT Companies, opines that there is a strong need to formally address the ethical issues with all seriousness. She further adds that the Ethical and Compliance Policies are not in place in Indian IT Firms and there is a strong need to improve up to reach upto global standards, if they wish to succeed in global market over a long term. A standard for measuring and reporting ethical behaviour in business should be adopted to validate the claims of it being ethical.

Sharma (2014) further exclaims that Ethical Codes in the Indian Context have not been subjected to much scrutiny. She disserts that most Indian Codes, at present, are heavily rule based & complex, reducing the ease. She prospects that Indian Ethics' Code will move from mere compliance to a new value based sphere.

Kain and Sharma (2014) further recommends that by adopting the NHRC ( National Human Rights Commission of India) Code of Ethics, Indian Enterprises can lead hundreds of MNCs that have adopted the United Nation's "Protect, Respect and Remedy" Framework.

Mishra et. al (2014) observes that most of the well established firms have a well written ethical code of conduct and they strictly follow it. These firms are successively increasing their participation in the CSR activities. Whereas, the small start-up firms stress on revenue collection.

Kshatriya (2014) exclaims that business world across globe has started looking east, particularly India, for Ethical Business Models. He suggests that a culture that is conservative in monetary terms attaches a very high value to created wealth, in turn, leading to business practices bringing change in lives of many and ensuring the process of wealth creation.

Patel and Schaefer (2014) further argue that choices about specific ethical behaviours do not depend on static and universal set of rules. They suggest that four predominant types of ethical behaviours coexist in every social system, linked to the dynamic coexistence of the four solidarities or cultural patterns, especially in Indian context. It implies that managers from one national background show greater ethical awareness than that of others having a variant. They further suggest that ethical codes created in the context of one cultural pattern are unlikely to be accepted by employees having the different cultural backlogging and thereby difficult to implement. Further no one strategic business model, code or approach is applicable in this world in all respects in all business entities.

They further recommend that more empirical and theoretical research work is needed in the sphere, to firm up the exact modular relationship between the societal culture and business ethics.

All these works reveals us the importance of ethics and depicts out the need of ethical business practices to upgrade the position, but due to competitive business environment finding, it is hard to do so. At the end of this chapter, we will only say that this not a exhaustive list of the research work happened and only commits to bring a brief picture on the research works done by some of the most eminent.

2.1 Research Gap

As described in the literature review, good work is being done at the world level. In case of Asian perspective a less number of researches had found taken place. But we have found a least or negligible no. of research work done on the phenomenon with regard to India in a rigorous manner. Only a few reports or papers are found in this behalf. In this research, we will try to cover the same research gap by using different data sources relevant to the study.

2.2 Feasibility Study

As discussed earlier, this research depicting the problem and its solution tends to have an interpretation of the Existence and Practicability of Ethical Conduct in the Present Competitive Business Environment of Indian Business Houses, especially in Services. Its need can be judged from the thing that the problem is of substantial importance on account of the corporate governance practices opted by Indian firms as a part of global economy as well as not as such significant work being done on the above said phenomenon. This study will be a significant study, as it will give a clear picture of the collective scenarios of Indian Businesses in this context and make a useful contribution towards the analysis of the phenomena.

RESEARCH METHODOLOGY

3.1 Research Design / Methodology

There will be a three tier study for the purpose. At First, Key Personnel(s) / Official(s) of the above Organizations will be interviewed / surveyed by the above mentioned modes of data collection, as its internal stake holders. they will be asked about the existence of EBP in corporate world and their organisation, the details of EBP opted by their concern for its service delivery, and the impact of such EBP on the organisational and business growth of their organisation. Secondly, Customers in reach, nearby observers, Government representatives, Independent Company Auditors, Independent Research Organisations, Research Groups, CSR / Corporate Governance Organisations, etc. with questions about EBP in service delivery quality and service failure handling, as the external stakeholders. Besides an independent but relevant study about ethical services delivery will be conducted from the general public available at public places, with a sample of 60 Respondents Each from the given Three Corporate cum Metropolitan Regions / Circles of Bengaluru - Hyderabad - Chennai, Delhi NCR, Mumbai - Pune - Ahmedabad.

Being a Qualitative Research, design opted for this research will be Descriptive Research Design, where Survey will be the Primary Method of Data Collection. For the purpose of Primary Data Collection, Structured Data Collection Design of survey method will be used with the majority of Close-Ended Alternative Design of Questions in the questionnaire.

For the Purpose of Interviewing, Primarily Personal Interviewing with a supplement of Telephonic & Electronic Interview Techniques of interviewing, will be used, depending upon the reach and availability of sample. In some cases, Observation will be used as a supplementary source of data collection whenever applicable. A Pilot Survey on 5 Percent of the Sample, i.e., 10 Organizations, will be initiated in inception to leash out the anomalies left, which will be followed by Main Research Survey, after corrections, in the respective sub-sectors.

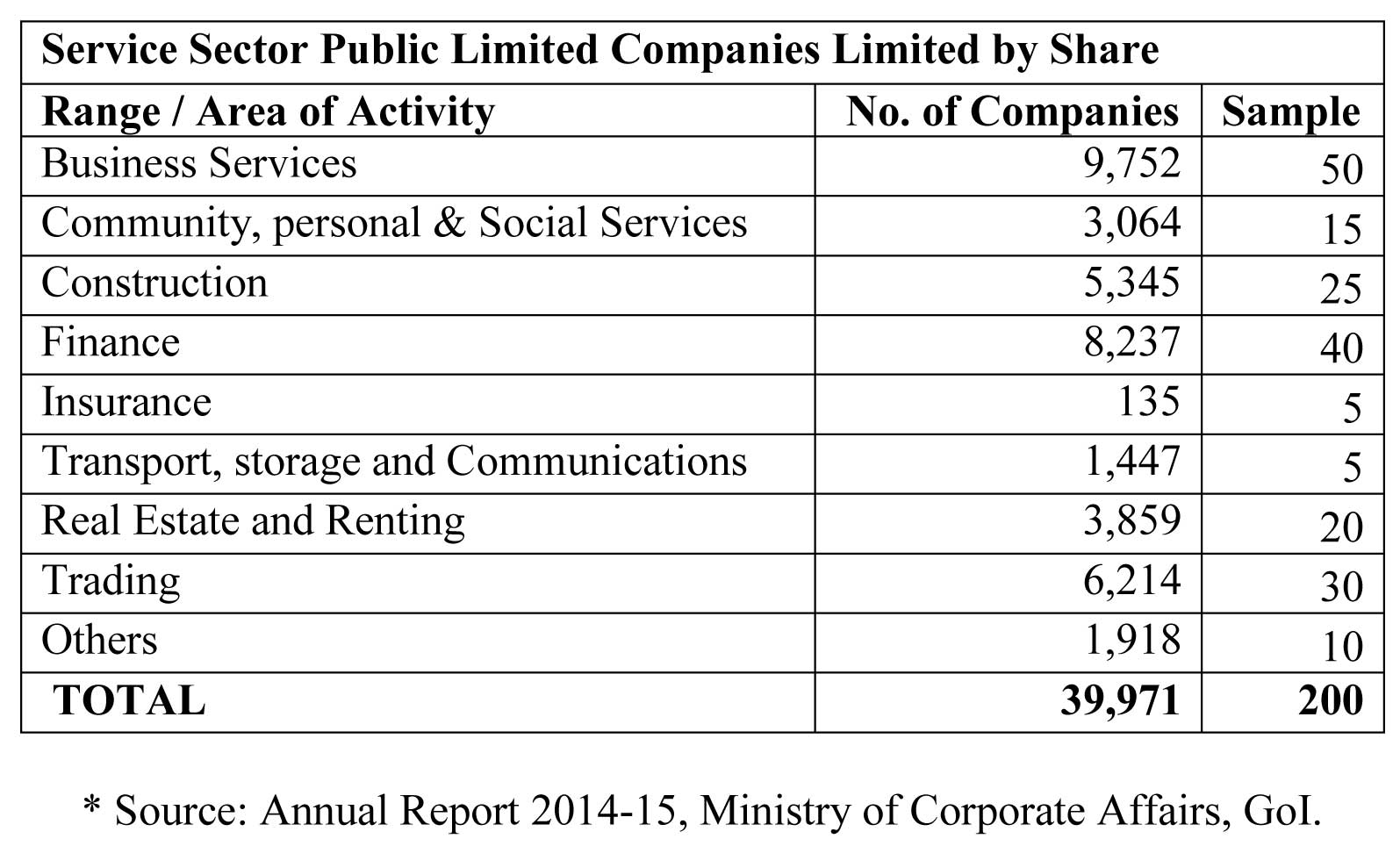

Methods for the data collection from the above sources will include Sample Survey, Observation, Expert Opinion and Secondary Data Analysis as appropriate with a Sample Size of 0.50 % (all India sample of 200 Concerns out of Total 39,971 Concerns in Service Sector India*), adjusted based on adequate representation of the industry and region.

3.2 Measurement and Scaling

For questioning in survey questionnaire rating scales such as category scales, summated rating likert scale, and graphical rating scale will be used for the purpose. Dichotomous questioning will be used for some of the basic incepting questions such as to ask about the existence of ethical governing structure in the organization.

3.3 Sources of Information

For preparing project report different types of information will be collected from different sources. The main sources for this purpose will constitute:

- Primary Sources: These are those which are collected and used for the first time by user. The primary sources of this project report include primary market survey, various meets, interviews & seminars with the various economists, analysts, industry and spokespersons (relevant and accessible) of respective fields as well as general condemn of society at large.

- Secondary Sources: These are the sources, which have been used and reused by user for specific purpose. The main secondary sources for this project work data and other facts collected through internet, news paper and journals reports and statistics of various organizations which include annual reports, special reports, surveys and facts of analysis etc.

3.4 Sampling Criterion

For the purpose of sampling, companies / other registered organizations in service sector, having its span of operations in India will be considered as population. For the purpose of primary data collection, a proposed sample size of 200 Service Concerns PAN India is taken into consideration.

3.5 Sample Size

For the purpose of primary data collection, a proposed sample size of 0.50% is taken into consideration. Apart every detail of primary data collection, subjects to change and modification depending on the subject of relevance and reliability as well as feasibility. The details of Survey, in respect of regions & samples, will be covered as follows:

Note 1: Population, here for the purpose of this research consists of Service Sector Public Limited Companies Limited by Share in the respective activity. Since the population being large & bigger concerns have a more probability of getting indulged in unethical practices (well proven by researches), thereby in order to make survey representative of the actual, the focus of population will lie especially in large and medium scale of business concerns. Sectoral quota as well as Industrial regions will also be considered while determining the size of sample, based on share of each sector / region in the total investment as well as contribution to the GDP growth of nation, which will be interpreted later in thesis. Where sample is less than five then it had increased to five, to ensure the common opinion. Figures rounded-off to nearest multiple of five, to facilitate ease of reference and calculation. No Pilot Survey will be conducted in the Ranges, where the Sample Size lies below 20, i.e., Sample Size limiting the Condition of Calculation of 5 Percent of Sample.

Note 2: An additional study will be conducted from the general public regarding their opinions on Services Reliability and business ethics, with a sample of 60 Respondents Each from the Three Corporate Metropolitan Regions of Bangalore - Hyderabad - Chennai, Delhi NCR, Mumbai - Pune - Ahmedabad.

3.6 Sampling Technique(s)

Stratified random sampling will be used for the purpose of sampling, with a supplement of simple random sampling. Judgmental and/or convenience sampling will be used in exceptional cases.

3.7 Statistics Proposed to be used (All India Basis)

‘NIIR - All India Companies Directory - 6th Edition’, well providing about the key official(s) as well as other necessary details will be used for the purpose of statistics for allocating sample out of above mentioned population. Besides, other significant statistics will be used to supplement it.

3.8 Data Collection Technique(s)

For the purpose of primary data collection, data will be collected through personal interviewing wherever desired as well as within the reach of researcher, with a supplement of enumerators/mail questionnaire / e-mail interview / questionnaire / etc.

3.9 Sampling Variable

Key Personnel(s) / Official(s) of the above Organizations, as per the proposed statistics, will be interviewed / surveyed by the above mentioned modes of data collection. A sample draft of Questionnaire / Survey Form is annexed therewith at the end of this document.

ANALYSIS & INTERPRETATION

4.1 Tools and Techniques of Research Analysis and InterpretationAll Applicable Tests and Tools of Statistical and Behavioural Economic Analysis, such as Tests of Significance and such other Tests of Hypothesis, among others, will form the part of Tests and Analysis used during the study. Other Tools, such as Analysis of Interdependence, Discriminant & Logit Analysis, Multidimensional Scaling & Conjoint Analysis as well as Correlation and Regression will supplement the analysis, for the purpose of study. Further, Structured Equation Modeling & Path Analysis as well as Chi-Square Automatic Interaction Detection (CHAID) Technique is proposed to be used for the purpose of analysis. Statistical Software Tools as well as other necessary computing & manual amenities will be used for the analysis and preparation.

4.2 Thesis Presentation / Tentative Chapterization of Thesis

Presentation and Format of the Final Thesis and other supplementary reports will be based upon the studied format of earlier reports on various subjects, acquired academic as well as professional knowledge, and the overall instructions and specifications made by the Academic Guide as well as other faculty advisory available at University / elsewhere. The main components of the report will consist of:

- Introduction (to the topic);

- Review of Literature;

- Research Methodology;

- Analysis & Interpretation about the research; &

- Conclusion & Recommendations drawn out.

- References / Bibliography

- Tables, Graphs & Figures After the preparation of report, hard copy(s) of it will be submitted to the University Offices, as per the given specifications. Seminar presentation will be held at the institution premises, at the convenience of faculty. After due feedback and discussions, the study will stand completed.

4.3 Limitations of the Study

Being a relative analysis, the research does not tend to present the relationship between ethical practices and business growth in absolute terms; rather it expresses a relative relationship between both these variables. Hence, it may be a limitation for the purpose of future budgetary forecasting. Further, as this research will be only on Indian Business Houses in Services; hence, this will not comment out upon its need and status around the globe as well as remaining sectors in India. Besides, other information mentioned herein is wholly based on the available facts and figures, and it gives us an overview of the global scenario of ethical business practices based upon the data accessed. There may be a stance of probable errors and/or unintentional mistakes or misrepresentations in the preparation and presentation of the report.

References

- American Psychological Association (1992), “ Ethical principles of psychologists and code of conduct”, American Psychologist, Vol.47, pp.1597-1611.

- American Psychological Association (2001), “Ethical principles of psychologists and code of conduct (Draft for comment)”, The Monitor of Psychology, Vol. 32 (2), pp.77-89.

- Barnett, M. L (2007), “Stakeholder influence capacity and the variability of financial returns to corporate social responsibility”, Academy of Management Review,Vol. 32, pp.794-816.

- Blowfield, M (2003), “Ethical Supply Chains in the Cocoa, Coffee and Tea Industries”, GMI, Vol.43, pp.15-24.

- Campbell, K., & Malan, D(2002), “ Business ethics essential for viability”, Creamer Media’s Engineering News, Apr.

- Carr, A (1968), “Is Business Bluffing Ethical?”, Harvard Business Review, Jan-Feb.

- Carroll, A. B., & Shabana, K. M (2010), “ The Business Case for Corporate Social Responsibility: A Review of Concepts, Research and Practice”, International Journal of Management Reviews, pp.85-105.

- Collier, J., & Esteban, R (2007), “ Corporate social responsibility and employee commitment”, Business Ethics: A European Review, Vol.16, No.1, pp.19-33.

- Cory, J. (2005), “Activist Business Ethics”, Vol.9, No.11: Springer, Boston.

- Drucker, P (1981), “ What is business ethics?” The Public Interest, Vol.63, Spring, pp.18-36.

- French, P. A (1979), “The Corporation as a Moral Person”, American Philosophical Quarterly,Vol.16, pp.207-215.

- Green, R (1991), “ When is "Everyone's Doing It" a Moral Justification?”, Business Ethics Quarterly,Vol. 1, No.1, pp.75-93.

- Jalil, M. A., Azam, F., & Rahman, M. K (2010), “Implementation Mechanism of Ethics in Business Organizations”, International Business Research, pp. 1-11.

- James, H. S. J (2013),“The Ethics and Economics of Agrifood Competition”, Agriculture Journal.

- Kahneman, D., Knetsch, J., & Thaler, R (1986),“Perceptions of Unfairness: Constraints on Wealth Seeking”, American Economic Review, Vol.76, pp.724-741.

- Kain, P., & Sharma, S (2014), “Business Ethics as Competitive Advantage for Companies in the Globalized Era”, Journal of Management Sciences and Technology, Vol.3, No.1,pp. 39-46.

- Maitland, I (1994), “The Morality of the Corporation: An Empirical or Normative Disagreement?”, Business Ethics Quarterly, Vol.4,pp. 445-458.

- Mishra, N., & Sharma, G (2010), “Ethical Organization and Employees”, Asian Journal of Management Research, pp.79.

- Mulla, Z (2003), “Corporates in India Cannot Afford to be Ethical”, Management Labour Studies, pp. 1-7.

- Nainawat, R., & Meena, R(2013), “Corporate Governance and Business Ethics”, Global Journal of Management and Business Studies, Vol. 3, No.10, pp.1085-1088.

- Pal, A. M (2009), “Ethics in Corporate Governance: A Critical Review”, Journal of Business & Economic Issues,Vol. 1, No.1, pp.84.

- Pivato, S., Misani, N., & Tencati, A(2008), “The impact of corporate social responsibility on consumer trust: the case of organic food”, Business Ethics: A European Review, Vol.17,pp. 3–12.

- Preston, D(1997), “Can Business Ethics Really Exist? “Computers and society, March,pp. 6-11.

- Rebelly, H., & Ragidi, V (2014), “Ethical Issues in Business & Corporate Governance: A Case Study of NTPC- Ramagundam”, International Journal of Marketing, Financial Services& Management Research,Vol. 1, No.5, pp.62-67.

- Seshadri, D. V. R., Raghavan, A., & Hedge, S (2007), “ Business Ethics: The Next Frontier for Globalizing Indian Companies, Vikalpa,Vol. 32, No.3, pp. 61.

- Sharma, M (2014), “Ethics Statements on Web sites of Indian Companies”, Research and Publications, W.P. No. 2014-05-01, pp.15.

- Stark, A (1993), “ What's Wrong With Business Ethics?”, Harvard Business Review, Vol.71, No. 3, pp38-48.

- Sunstein, C. R (2002), “Switching the Default Rule”,New York University Law Review,Vol. 77, pp.106-134.

- Velasquez, M (1983), “Why Corporations Are Not Morally Responsible For Anything They Do”, Business & Professional Ethics Journal, Vol.2, pp.1-18.

- Κanungο, R., & Mendoca, M (1996), “Ethical Dimensions of Leadership”, SSBE Sage Series on Business Ethic, pp. 81.

- Freeman, R. E., York, J. G., & Stewart, L (2008), “Environment, Ethics, and Business”, Bridge Paper: Business Roundtable Institute for Corporate Ethics.

- Smart, V., Barman, T., & Gunasekera, N (2010, Oct),“Incorporating ethics into strategy: developing sustainable business models, CIMA Discussion Paper, pp.1-15.

BOOKS, CHAPTERS IN BOOKS, REPORTS, ETC.

- Behrman, J. N (1988), “Essays on Ethics in Business and the Professions. NJ: Prentice Hall.

- Clarke, T (2004), “Theories of Corporate Governance: The Philosophical Foundations of Corporate Governance”, London - New York: Routledge.

- DeGeorge, R. T (1999), “ Business Ethics, Prentice Hall.

- Donaldson, T (1982), “ Corporations and Morality”, NJ: Prentice Hall.

- Dunning, J. H., & Wales, P(2004), “Making Globalization Good: The Moral Challenges of Global Capitalism, PhilPapers.

- French, P. A (1995), “Corporate Ethics”, Florida: ICSA Publishing.

- Harwood, S (1996), “ Business as Ethical and Business as Usual”, CA: The Thomson Corporation, Belmont.

- Husssaini, N (2014), “Corporate Ethics of Top IT Companies in India”, Bhagalpur: TMBU Bihar India.

- Jones, C., Parker, M., & Bos, R (2005), “For Business Ethics: A Critical Text”, London: Routledge.

- Knight, F (1980), “The Ethics of Competition and Other Essays”, University of Chicago Press.

- Michalos, A (1995), “A Pragmatic Approach to Business Ethics”, London: Sage Publications.

- Mishra, A. K., Dalvi, B. B., Sahni, S., & Verma, V (2014). “ Ethical Considerations in Business Decision Making in Indian Companies” Mumbai: IIT Bombay.

- Seglin, J. L (2003), “The right thing: conscience, profit and personal responsibility in today's business”, NH: Spiro Press.

- Singer, P(1991), “A Companion to Ethics”,MA: Blackwell & Malden.

- Solomon, R (1991), “Business Ethics. A Companion to Ethics”, MA: Blackwell, Singer & Malden.

- Solomon, R. C (1983), “Above the Bottom Line: An Introduction to Business Ethics “, Harcourt Trade Publishers.