Subscribe now to get notified about IU Jharkhand journal updates!

Strategy for Venturing into the Unknown with System Dynamics Approach: Case study of a diversified company

Abstract :

The idea of Corporate Social Responsibility (CSR), its concept, philosophy and its importance to the encompassing society of any organization isn’t a totally new concept for the Indian Companies. Even before independence, we had many companies and organizations in India, who operated their business with social responsibility & some philanthropic aspects. We now know that the essence and spirit of CSR is that, the corporates should voluntarily demonstrate their concerns towards the environmental , social, philanthropical , ethical & other sustainable issues simultaneously, together that on profit, and creating wealth for the owners , shareholders and stakeholders. The concept of overall stakeholders’ satisfaction & reciprocating back to society has now gained permanency. This has happened all the more important due to the provisions in the companies Act 2013, through Section 135 related to CSR activities. Corporates have now realized, that CSR is now not only a statutory provision, (for those corporates to which it has been made applicable), but also that its success & existence in future will depend a lot on the stakeholders view about its CSR initiatives. Many Companies are spending even more than the statutory requirement of 2% of average net profits of the last 3 preceding years. But we still have a long way to go. It is also seen that though there is plenty of information available on CSR spending of companies in India (particularly after introduction of section 135 in the Companies Act 2013) very little is known about the impact of their CSR practices & spending in the society on the target groups or on the beneficiaries. The main contribution of this paper is a structured review of the development of the concept of CSR and it highlights how the societal expectations, constructs & statutory framework of CSR have evolved particularly in India.

This article emphasizes the journey of the concept of CSR in India right from the 1st phase to its present position as a mandatory provision in the form of statute under section 135 of the Companies Act, & the experience after its implementation in India, and the way ahead. It also highlights the challenges faced during the covid-19 pandemic for utilization of CSR Provision and the emerging areas in which one may invest in the current scenario.

Keywords :

Corporate Social Responsibility, Companies Act 2013, Impact Assessment. Corporate Culture, CSR Standards1. Introduction

In the Corporate World, particularly in India, now after the enactment of Companies Act 2013, Section 135, Corporate Social Responsibility is being discussed at all forums. It has assumed such importance that it is being now considered as the main fulcrum through which a company can derive multiple objectives towards sustainability on most fronts. The concept of CSR has now taken a paradigm shift from philanthropy to actual stakeholder engagement and reciprocation to the society by the corporates. Weare now experiencing the results of CSR implementation at ground level. Plenty of ancillaries are developing as facilitators and support services towards implementation of CSR schemes, projects in line with the CSR Policies of Corporates. CSR Planning, CSR Funding, CSR due diligence, CSR Audit, CSR Standards , CSR Disclosures, CSR metrics are all being documented, analysed and changes are going down on all these areas. New areas of implementation in line with the Schedule VII of the Section 135 are emerging and are also under the active consideration of the Government for inclusion within the CSR activities. Covid-19 pandemic has also detached a bunch of activities which are now recognized and eligible as CSR activities by the Government Of India. The experiences and learning from the CSR implementation within the last seven years has led to new insights into the role, importance, and further requirements of CSR activities. Lots of changes are being suggested and is the need of the hour ,so that the businesses and the corporates can actually join hands in hand with the Government towards the sustainable growth of the economy and the Society. At the end we discuss about the gaps in the implementation of CSR activities with special reference to the area of impact assessment. It is felt that very little thrust has been given to assess the real impact of the CSR activities on the society, in India, and a lot needs to be done towards developing CSR Standards, benchmarks, CSR index, metrics and the disclosure formats for measuring the impact of CSR activities in various sectors of the economy. The article in this sense is a very comprehensive compilation of all pertinent issues relating to the subject of CSR in India’s perspective considering the developments till date and the way ahead.

Review of Literature:

E, Ten Pierick, V. Beekman, C.N Van der Weele, M.J.G Meenseen, & RPM De Graff(2004)in “ A framework for analysing Corporate Social Performance- Beyond Wood Model” states and gives the conclusion that most operationalisations are not balanced in the way they treat policies, programmes, and impacts. Ideally, a performance measurement instrument should pay attention to all these aspects of CSP narrow and check for the consistency between them, i.e., are the programmes in line with the policies of the organisations and do they really lead to the desired impacts? In practice, however, we notice that there are some issues that are measured as policies and others as programmes or impacts. Moreover, it appears that convenience is one of the primary reasons for the selection of certain indicators by the organisations worldwide.

The FSG Co Founders – Michael porter, Professor of Harvard Graduate School & Mark Kenner first introduced the concept of CSV ( creating Shared Value)in “ Strategy & Society” in their (2006) Harvard Business Review article . CSV actually refers to examining in details the linkage between economic and societal progress. Much of India’s CSR initiatives & activities have manifested as philanthropy that targets well being of local communities around the places of their business operations. While these efforts & initiatives have definitely yielded some results, they have been rarely able to achieve large scale societal impact & sustainability in the long run.

Srinivasan (2007) in his article “ Corporate Social Responsibility” “states that CSR actually means sustainable development of the society by being an inherent part on their progress. In spite of a number of schemes and measures initiated by the Central & State Governments the actual benefit has not percolated to the target group. The Corporates can act as the “ last mile connectivity” facilitators & mediators. Thus CSR can act as a catalyst in unlocking the last mile connectivity for various types of social development”. Srinivasan (2007) in his article “ Corporate Social Responsibility” also underlines that CSR is more than just a generosity & does not only mean “ giving and receiving”.

Wood. J Dona in her article” Measuring Corporate Social Performance”:(2010) A Review :Blackwell Publishing Limited and British Academy Of Management. highlights about the fine differences between CSR and CSP. She elucidates that CSR is a part of overall broader concept of CSP(Corporate Social Performance), and stresses on the need for scholars and researcher’s to focus more on the stakeholders and society to assess the actual impact of Corporate social performance.

NeharikaVohra& Rahul Sheel in their article CSR practice, Theory & challenges (2012) has stated that “ Though CSR as a concept has gained immense popularity there is still a lack of agreement on what it really means. There are different expectations from different stakeholders groups, different standards,& different practices leading to a fragmented understanding of CSR.”

Niraj K Lal & Archana Dutta (2012) in their article : An Arvind Limited SHARDA TRUST initiative to Help the Urban Poor says “ The major challenge that we see in CSR today is that it is still being considered as an Act of charity and philanthropy rather than a strategy to improve a corporations competitive edge”.

Ananya Mahadevan (2012) in his article CSR at Coco Cola states “Sustainability is at the core to our business continuity and depends on how we create long term value from CSR”

Vijayta Doshi & Pradyumana Khokle (2012)in their article “ An Institutional perspective on CSR” emphasizes on the point that “ inefficient legal systems & loose monitoring of government regulations leave scope for various degrees of compliance to the Acts by the organizations resulting in socially irresponsible behavior of the organizations”

VasanthiSrinivasan(2012)in her article “Developing a responsible business course for business schools in India”tells about the Primary objective of a course on responsible business in management school curriculum would be to stimulate critical thinking amongst young managers about their roles as professionals in business organizations in the larger context of sustainable growth of the society and the economy..

Lalitha Vaidyanathan and Melissa Scot(2012) in their article “ creating shared value in India: The future of inclusive growth” has highlighted that India Inc is not only uniquely placed to be in the forefront of economic development but will also contribute to a large extent in transforming organizations to create shared values in a change process” . Though it will take time, effort & persistence but will definitely bring results both for the business and society”.

Sasmita Palo &RohanSharma(2012) in their article “ From Indiscriminate Shooting by Corporate Hunters to creation of Responsible “Boom E Rang Society”has stressed upon a very unique concept that just like a boomerang comes back to its original destination, a model needs to be developed wherein the corporate hunter is held responsible & accountable to give back to the community , environment and society all that or partly what it has extracted from it.

Ghuman (2013) in his article “CSR: An effort towards inclusiveness & equity “revealed that the clause 135 of the Companies Act 2013 could be a milestone in the growth story of India. He stated that the quantum of cash to be invested in CSR activities due to the mandatory provisions of Sec 135,are going to be in billions of rupees. If invested & utilized with sincerity & honesty, it can generate brilliant results & have a positive impact on the Indian Society.”

Dhanesh, Ganga. S. (2014) has examined CSR as a management strategy that might strengthen relationships between organizations & stakeholders. The Study also establishes a powerful relationship between CSR & organization -employee relationships, especially between legal, ethical & discretionary dimensions of CSR”

Singh & Sharma (2015) in their article “ CSR practices in India: Analysis of Public Companies” explains the regulatory provisions and structure of the CSR policies and activities meted out by two PSU’s namely CIL and GAIL. The initiatives are particularly within the area of health, sanitation, education, women empowerment, nutrition, and rural development. The research of this text reveals that not only are these two companies working tremendously for CSR & covering areas covering under Schedule VII of sec 135 of the Companies Act 2013, but also beyond such areas.

Singh Priyanka (2016) in her paper” CSR, Its roles & Challenges in Indian Context “discusses the role of CSR together with the main issues/challenges faced by the Indian companies& suggests remedial measures for effective implementation of CSR activities.

Chatterjee & Mitra (2017) in their article “ CSR should contribute to the national agenda in the emerging economies”-stresses upon the “Chatterjee model” of implementing CSR initiatives. The Chatterjee model lays emphasis on projectivization of CSR activities ie implementing the CSR activities through the project mode.

Dr P. Srikanth (2018) in his article “CSR performance & advertisement expenditure & its impact on revenues of the Companies” states that CSR performance can’t create fortified brand image for the firm unless it’s effectively showcased to the customers through advertisement.

NantuRanjan Pal (2018) in “CSR- a dynamo generating basic amenities for low lying societies” states that there has been an enormous achievement that CSR campaign attained down under the scheme of corporate governance is without any doubt. It is gradually crystalizing into the nature of a self propelled dynamo that would generate basic amenities for the low lying societies in continuum”

Kalyani Karna (2018) in her article “ CSR -moving from “I” to “ WE” to create new India tells that “ together we can make great things to happen & do the miracle. Government Professional institutions, researchers , employees & public at large can come together & synergize their energies to bring the societal changes”.

Objectives of the study:

A )To study the CSR Trends in India from early days ie the first phase to the current position

ie the current pandemic scenario.

B) To suggest ways for further learning from the past & present experiences.

C) To suggest the scope for further research within the field of CSR practices in India.

Concept of CSR& its evolution along with its linkage with Sustainable development Goals(SDG’s).

According to the United Nations International Development Organization (UNIDO) CSR is “ a management concept whereby companies integrate social & economic concerns in their business operations and interactions with their stakeholders”. CSR is generally understood as one of the main fulcrums and means by which a company achieves anequilibrium of larger economic, social and environmental imperatives”. This is what is commonly known as the Triple bottom line approach, while at the same time addressing the expectations of the stake holders and the shareholders.Industrial houses like Tatas, Birlas have been contributing a part of their profits to their charitable Trusts since their inception. This they did at that point not because it absolutely was legally required, but it was the right thing to do for the society. Then came the welfare approach. Many Indian public sector entities engaged themselves in labour welfare and community services voluntarily. It embodied the notion that those who were in a position of strength and privilege should do something for the weaker sections of the society and the needy. Hence, we see that few Indian businesses have been traditionally socially responsible, but this culture has to be now deeply percolated and must flow in the lifeline deep into the roots of Indian corporates and the business world.

The Ministry of Corporate Affairs (MCA) Government Of India, released a group of guidelines called the National Voluntary Guidelines which were an advisory towards social, environmental and economic responsibilities of business.(referred to as National Voluntary Guidelines : NVG’s) so as to align and converge the NVG’s with the Sustainable development Goals (SDG’s)of the United Nations Guiding Principles .The process of revision of NVG’s started from 2015. After its revision &updation the NVG’s are now called the NGRBC, (National Guidelines on Responsible Business Conduct). These are supportive and voluntary guidelines which acts as a policy guideline to assist businesses beyond the actual regulatory requirements. Businesses cannot prosper in an environment of poverty, violence, inequality and environmental degradation. Hence the concept of doing well for itself and also the society at large towards sustainable development gained importance.

The 2030 Agenda for sustainable development adopted by all member countries in 2015 states the blueprint for peace , prosperity and sustainable development goals. At the centre stage is the 17 SDGs, the (Sustainable Development Goals) which basically are the pillars towards the formation of the various statutes developed towards CSR in India and many countries worldwide.

India is the first country in the world to make CSR mandatory, through legal provisions of law . In the Indian Context too, the CSR provisions and CSR spending areas can be correlated with the 17 SDGs. Each of the areas prescribed in Schedule VII are coherent with the SDG’s. (Sustainable Development Goals). Also the principles enshrined in the NGRBC can also be mapped with the SDGs (Sustainable Development Goals).

The Linkage of CSR &Corporate Governance

Corporate Governance is the application of the best management practices and principles, compliances of law in letter and spirit, and strict adherence to ethical norms and standards for efficient distribution and management of wealth and effective discharge of social responsibility towards sustainable development of all. As is evident form the stated definition, Corporate Governance has CSR embedded into its bloodstream. The basic premises is that when a company gets bigger in size, apart from the basic objective of earning profits and creation of shareholders wealth, there are many more responsibilities attached to it, which are purely social in nature. Companies that practice good corporate governance are also the ones that have good CSR practices embedded in their system. Unless there is a good and strong corporate governance, it is quite unlikely that there is a consensus towards social responsibility. Businesses are recognizing and realizing that, an effective CSR approach can minimize business disruptions, and enhance brand reputation both at national and global levels which also helps in attracting capital and technology.

CSR & other similar related concepts

We , sometimes get confused with CSR and other similar topics like corporate sustainability, philanthropy, Corporate citizenship, ethical business actions, Corporate Social Performance etc . Hence the confusion should be cleared at the first instance. Philanthropy is basically an act of charity, generosity and helpfulness by and giving financial contributions either in cash or kind without being actively involved outside the funds offered.CSR on the other hand, goes much further by directly involving itself in the causes, concerns and the community. Corporate citizenship is another concept whereby businesses form an integral part of business culture. As a part of good corporate business, the corporates focus on creating value for the society , ethical & equitable corporate practices, eco efficient systems and creating market for all. The concept of corporate sustainability is the capacity of a firm to create value through its products and services, and continue operating for years with profits . Corporate sustainability includes an attempt to assimilate environmental, social dimensions into business operations, processes, products, procedures. Although Corporate sustainability and CSR have different roots and background and different pathways, initially, both of them have ultimately converged.

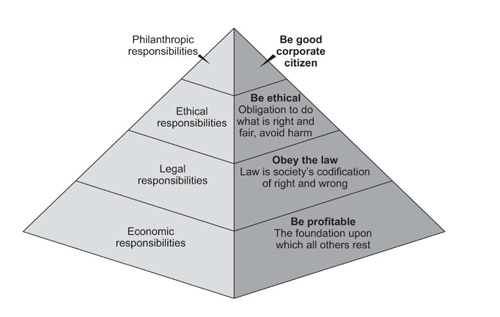

The carrolls pyramid developed by Archie Carool highlights how the CSR has developed into a pyramidal structure. It tells us about the four main responsibilities of business ie the economic (ie to make profits), Legal (ie to comply with the statutory obligations) the ethical ( ie to do what is right for all, just & fair and avoid harm) and lastly Philanthropic responsibilities( ie to be a corporate citizen, improve quality of life at society to the extent possible by corporates).

There is another concept of CSP (Corporate Social Performance) as propounded by Woods which focusses on the impacts and outcomes of corporate performance on society, stakeholders and firms.

The legal & statutory structure of CSR in India

The Government of India has enacted the Companies Act 2013 (August 2013). Section 135 of the Act , deals with the topic of CSR. The section 135 together with the CSR rules (2014) and Schedule VII of the Act provides the essential framework towards CSR. As per Sub section (1) of Section 135 CSR is applicable to every company which fulfils any of the three conditions prescribed ie a) having Net worth of Rs 500 Cr or more b) having a Turnover of Rs 1000 Cr or more c) Net Profit of Rs 5 Cr or more. Every Company covered under sub-section (1) of section 135 shall constitute a CSR committee of the Board consisting of 3 or more directors with at least one independent Director. Where, however, appointment of Independent Director is not required as per mandate, then the CSR Committee may consist of two directors only. The CSR Committee ,through the Board will ensure formation of a CSR Policy along with monitoring the Budgeting, expenditure and Reporting in terms of Annexure -I as prescribed under the Act.

Schedule VII of the Act prescribes the main heads of activities which might be undertaken under the Act and supported with the CSR policies of a company . The items listed in Schedule VII are broad based and are to be understood liberally. However, in determining and finalizing the CSR activities, preference shall be given to local areas , around which the company operates.

It may even be noted that before the implementation of CSR Provisions as per the section 135,we had the DPE (Department of Public Enterprises) guidelines applicable for central PSEs. These are in the nature of guiding principles and guidelines.These DPE guidelines are still applicable to Central PSEs but are in the nature of recommendary guidelines only in addition to compliance of Section 135.

As far as Insurance Companies are concerned, the prescription as mandated in Section 135 is applicable to the Insurance Companies. As regards private Sector Banks, since they are incorporated as Banking companies, CSR Provisions as per Sec 135 is applicable. However, Nationalized Banks are not incorporated as a Company under the Companies Act 2013, and are hence not coveted under the CSR provisions of the Companies Act Section 135. They are however , required to spend 1% (maximum)of their Net Profits, through donations, as per the RBI regulations.

Implementation of CSR policies, the ways & means:

The applicability of the CSR provisions for a company begins, the moment the provisions as per section 135(1) is triggered. The CSR committee as formed by the Management is responsible for planning, executing, monitoring, evaluating and communicating the report, evaluation and the impact of CSR programs and communicating it to the Board. The steps involved towards this direction are:

i)Triggering of CSR provisions. ii) Motivate Top Management iii) form CSR Core group/CSR Committee iv) identify focus areas /major areas in line with scheduleVII of the Act. v) Design & implement the CSR action plan. vi) Monitor& evaluate the CSR actions and the impact to the target groups. vii) Monitor & report the CSR initiatives

Mode of doing the CSR activities in most of the cases are as follows:

a) Through a company established under section 8 of the Companies Act

b) Collaborating with other companies

c) Through capacity building of its employees for CSR functions and works

d) Through NGOs (Non-Government Organizations)

e) Through creation of a Trust under section 3 of the Indian Trusts Act 1882.

Governance issues in CSR implementation:

The Governance of CSR activities is through the Board and ultimately through the CSR Committee or the CSR core committee. However , what is required is dynamic monitoring through CSR Project Management Approach, Stakeholder engagement, CSR Risk Management,& using CSR as Organizational brand building.

Monitoring of CSR activities.

The Company should monitor the CSR activities as per the CSR Policy of the corporate, both through internal & external means. The common methods employed in most of the cases are (though the list is not exhaustive):

a) Project (Activity ) Monitoring

b) Beneficiary monitoring

c) Organizational Monitoring

d) Financial monitoring

e) Compliances monitoring

f) Context (situation monitoring)

g) External Third Party Monitoring

h) Board level monitoring and also CSR/Core Group Monitoring

i) CSR Reporting

Compliance of Section 135 of the Companies Act 2013:

Since CSR is now mandatory as per section 135 of the Companies Act, it is necessary for the corporate, the Board and its management to be fully aware of its provisions so as to avoid any penal measures. The main points to be kept in mind are:

a) Display of CSR Policies and major activities in the Company Website

b) CSR Reporting as per format/disclosure details prescribed under the Act

c) Proper Accounting of CSR activities as stipulated in the Act

Due diligence of CSR Funding & spending

It is very important to have proper due diligence of CSR funding and CSR activities and spending. In addition to proper project monitoring, the principles enunciated by the Institute Of Company Secretaries Of India (ICSI)in November 2017 are to be followed for adequate due diligence. There are Nine principles for Code of Charity Governance. The major ones are a) Vision & Objectives b) Adherence to laws c) Effective Governing Body d) Diversity & Conflict Of interest e) Disclosures & Transparency f) Community Engagement, integrity & sustainability.

CSR Audit & CSR Standards:

The CSR Audit also called the social audit ,is a method to evaluate the performance of the corporates on the social front. The benefits of CSR Audit or the social Audit are manifold. They are as follows:

a) Makes the organization a socially responsible corporate citizen.

b) Optimizes resource allocation.

c) Branding and good image amongst the stakeholders.

d) Prevents environmental disasters, poor technology, poor quality products.

e) Helps to achieve economic ends through social means..

f) Checks compliances of statutes

Emerging areas in CSR:

Education & Health Care sector are the emerging areas in CSR Spending as can be seen from the various reports on CSR Spending and the annual reports of Companies for which the CSR is mandatory. An analysis of CSR spending from 2014-2019 shows that: the area of Health, Community Welfare & Education has been given the major thrust by most of the corporates. A lot of work now remains to be done in the area of Research & Development in the areas related to the Schedule VII areas and the pattern of spending.

Challenges faced during Covid 19 Pandemic and CSR activities implementation:

It is experienced that many companies have stopped or minimised on their unethical practices during this pandemic. On the contrary these companies have now started to be proactively engaged in activities in line with National & social demands to fight against the virus.No Doubt the pandemic has offered a lot of opportunities for many entities to show their mettle who have more acumen and approach towards CSR philosophy and integrated generic approach towards CSR. Hence it can be seen that Covid 19 pandemic has opened a plethora of opportunities for companies who want to actively engage in generic CSR activities and agendas. The point to ponder is that in spite of many firms at the brink of collapse or drastic reduction in business, many firms are , still going for socially responsible and ethical activities. This is an area of further research , because what drives firms to be more ethical when resources are restricted, there is friction in flow of capital and business, is not really understood.

The short term effect of Covid-19 has been felt both at the national & international levels due to the widespread effects of lockdown and social distancing. However, as & when the pandemic ends, it will have long lasting economic, social, political, & cultural impacts. Covid-19 has posed serious threats and challenges to organisations and companies worldwide, particularly with regards to CSR activities. It is seen that many firms have been unethically profiteering and encashing on the difficulties faced by people during this pandemic, leave aside implementing CSR activities and reducing long term CSR investment. There is another side of the coin too. Fortunately we have seen many companies coming out proactively with enhanced CSR engagement and CSR activities even during this difficult times, to bring immediate relief to its customers, stakeholders and general Public.

A firm’s genuine and authentic CSR, along with its generic CSR will build stronger rapport among its customers and the general public, because they have built up strong expectation from leading brands, particularly their favourable brands, during the current crisis with regard to their efforts in combating the pandemic. Consumers generally feel proud of their brands and companies helping their employees, donating money and equipment during the crisis and getting integrated with the society for planned activities for helping the needy. The bond established between the brand and consumer during this crisis period can be more meaningful and lasting than during “peaceful” times. Therefore, how can we convince the business leaders about the importance of CSR under mounting survival threats? There may be two contrasting viewpoints and predictions on this. On the one hand, firms may get discouraged from investing in CSR because of the necessity for firms to target their core operating business for short-term survival. On the alternative hand, history has told us that shifts in environmental forces viz oil crisis within the 1970s, famines, etc have facilitated the event of CSR.

Therefore, a more optimistic view is that Covid-19 pandemic will accelerate post-pandemic CSR development within the near future, as more and more firms and businesses realize that their long-term survival and development will ultimately depend on achieving a balance between profitability and harmony with its various stakeholders. Probably the more relevant and pressing question isn’t about whether to require an edge in CSR or not, but more about the way to invest in CSR to attain the mutualist beneficial and interdependent social/environmental and economic goals. Most of those points stated above shows that, there’s still higher level of inequality within the developed world in terms of wealth, financial inclusion, health, insurance facilities, education, and so on. This offers significant opportunities for CSR and also for businesses to grow vertically and diversify.

Way Ahead based on past and recent experiences.

Learning from the experiences after implementation of Section 135 of the companies Act 2013, and from the analysis of the CSR spends in the last six years , I can see that there’s an urgent requirement of devising ways for locating adequate standards, and benchmarks for CSR activities in India, and that too sector wise in terms of the schedule VII of the Act. Plenty of changes are also required within the statute through amendments in the Act and also within the rules. The main points which are to be considered may be summarised as follows:

a) Most of the businesses have spend their CSR amount in Education, healthcare , disaster management, women empowerment mostly, to mention some. Businesses end up spending in these common areas ,and that too in overlapping physical realms. It’s recommended that companies set out with the concept of pooling of CSR activities in a very kind of National /state wise alliance in order that better & efficient utilisation of resources can happen.

b) In the post liberalisation phase and also within the post implementation phase of the section 135 of the companies Act 2013, though there appears to be a paradigm shift from the philanthropic view to the concept of stakeholder oriented approach, much needs to be done at the implementation level which are flexible enough to fulfil the wants of the target community.

c) More & more participation of youth and students at University Levels is required so that they will be sensitized about the CSR concepts, CSR philosophy and therefore the need for proper implementation and impact assessment of CSR activities. It’s recommended that the combined participation of professionals and executives from Industry, students & researchers from academia and the NGOs and other implementing agencies may be explored so as to make the CSR programs and its impact more meaningful and impactful.

d) The Government should consider a system of rewarding & recognising good CSR programs and practices. This may lead to more voluntary participation of corporate houses in the CSR activities.

e) It is seen that most of the CSR activities are directed either to the Urban or semi urban areas which are located near the local boundaries of the factories, corporate houses. We all know that India still is in 70 % of the rural areas. Hence, more thrust should be given to implementing CSR activities in rural areas also.

f) The requirement of CSR activities as per section 135 mostly is applicable to big corporate houses and PSU’s. However a major chunk of SMEs and small scale industries are left out from the ambit of mandatory CSR provisions. Government should find out ways to bring SMEs also under the ambit of CSR so that it is ingrained into the core business activities of the corporates and businesses including the very important SME sector.

g) Rule 2 (e), 4 (1) provision to 6 (1) of Companies Act, 2013 mentions that activities in the normal course of business is not allowed as CSR initiatives. It means that a company, which is in the business of distance education, cannot do CSR in education, a pharmacy company cannot supply medicines free of cost; a hospital cannot provide free health care, etc. This rule is against the doctrine of business case of CSR. A hospital has the best expertise and resources for health care, a pharmacy company can distribute medicines at cheaper rates. Rule 2 (e), 4 (1) of Companies Act is understandably a precautionary measure to check the distribution of substandard product to needy. But, by better monitoring and auditing this difficulty can be overcome.

h) Relationship between CSR & organizational identification process can be another area of research , ie whether instead of having separate CSR wing in an organisation, every employee working in the organization must be involved in conceptualizing CSR initiatives. Mandatory volunteering and involvement of each and every employee in CSR activities will enhance already existing CSR thoughts and CSR culture. Organizations must involve most of their internal &external stakeholders in CSR implementation which will help creating firm image and brand. Managers while making decisions about CSR need to be more aware and considerate of stakeholders’ responses.

i) Indian firms generally do not tie up with academia for research & scientific advancement. I am of the opinion that such help would indirectly boost the manufacturing segment & in turn eradicate unemployment & poverty.

j) There should be standardised disclosure formats (including CSR Index and metrics) for measuring the impact of CSR activities in various sector.

k) The foundation of Corporate Social Responsibility initiatives/policy of the organisations is ethical orientation of the decision makers which cannot be imposed/improved through government policy. The same can be improved through education of Ethics and Values at school and University level. Success related to Corporate Social Responsibility initiatives/policy of Organisations demands strong synergy between the Decisions Makers of the Organisations and Investors viz. shareholders, bankers etc. failing which efficiency andeffectiveness of the initiatives will drop. The use of ethical oriented technology should be stretched all over the organisations for awareness regarding Corporate Social Responsibility initiatives/policy from Top to Lower level of Management

l) The traditional method of providing Corporate Social Responsibility support shall be replaced/optimized with the latest one, supported by technology for better return with low cost. By testing and learning from success and failure from project to project, activities to activities, improvement/changes shall be adopted.

m) There is no standard qualifications required to work in this field of CSR as CSR managers backgrounds vary due to diverse disciplines. Preferred Skills include environment management, ethics of business, technology transfer, Human resource Management, Finance, community development etc. However it is suggested that skill sets required to work in these area of CSR may be standardised which may lead to a new branch of study required for optimal performance in the area of Corporate Social Responsibility.

The suggestions mentioned above will definitely provide a win-win opportunity for organisational and societal goal inclusive of sustainable societal growth which can only be achieved through collaborative efforts.

Scope for further study:

I have mentioned the historical perspective and the experiences of implementing the CSR provisions , post enactment of CSR as per Section 135 of the Companies Act 2013. Though there are many studies and research being done on the impact and correlation between CSR spends and the profitability of firms & Companies as a Strategy towards improving the Income Statement and the Balance sheets of Companies, there appears to be very few literatures available on the ways and means to assess the actual impacts of the CSR activities on the target beneficiaries and the larger society . This exercise needs to be started now, both at the level of academia in Universities, Research Organizations and also at the Industry and Government level so that these studies can bring forth further reports for analysis of the policy makers and the academicians and researchers for evolving models and benchmarks that may be applicable across a wide spectrum of social parameters. The impact study can be for Private Sector, Public Sector or manufacturing sector , Service Sector,FMCG Sector, Power Sector, Energy Sector, Agricultural Sector or Geographical region wise. For assessing the impacts ,standards and benchmarks are to be devised so that the actual effect can be monitored and effective action be taken so as to find out the social benefits pre and post the CSR initiatives and implementation. There also remains a lot of scope in examining the disclosure practices throughout India regarding the CSR activities of Indian Companies, the metrics being used and the factors effecting the choice of CSR activities by the Indian Companies. Moreover, this area of CSR being multidisciplinary and multidimensional, will also be a favorite for researchers in social sciences. Experts from Finance, HR, Strategy, operations, marketing, and policy makers will get a lot of opportunities in this particular field for capturing the actual impact assessments of Corporate Social responsibility activities in the days to come.

A paradigm shift in corporate social responsibility thoughts, ideas, areas,practices , disclosures, metrics and all other factors effecting the broad ambit of CSR is now expected particularly in India considering the huge amount of resources and fund to be employed in this area , the statutory requirements and also the synergistic impact of the CSR activities along with the corporate and Government functions towards sustainability of the organization, economy and the environment.

References

- Agnisis, H., &Glavas, A. (2012). What we know and don’t know about corporate social responsibility: A review and research agenda. Journal of Management, 38(4), 932–968.

- Ananya, M. (2012). CSR at Coca Cola, Vikalpa. Print. SAGE Publications, 37(2, April–June);ISSN: 0256-0909, 2395-3799(web).

- Ante, G. (2016). Corporate social responsibility and organizational psychology: An integrative review. February 2016. Frontiers in Psychology. Retrieved from http://www.frontiersin.org, 7, article no. 144.

- Arora, B., &Puranik, R. (2004). A review of Corporate Social Responsibility in India.Development. Economic Times, 47(3), 93–100. doi:10.1057/palgrave.development.1100057

- Bhaskar, C., &Nayan, M. (2017). CSR Should Contribute to the in emerging economies -The Chatterjee Model”- International Journal of Corporate Social Responsibility, article: 1 ISSN: 2366-0074,(electronic)ISSN: 2366-0066(print)

- Bowen, H. R. (1953). Social Responsibility of the businesses.University of Iowa, Press.

- Brammer, S., Millington, A., &Rayton, B. (2007).The contribution of Corporate Social responsibility to Organizational Commitment. International Journal of Human Resource Management, 18(10), 1701–1719. doi:10.1080/09585190701570866

- Burke, L., & Logsdon, J. M. (1996). How corporate social responsibility pays off. Long Range Planning, 29(4), 495–502. doi:10.1016/0024-6301(96)00041-6

- Callaham, J. L. (2014) Writing literature review, A reprise & update .https. doi. org/10/1177/1534484314536705.

- Carroll, A. B. (1991). The Pyramid of Corporate Social Responsibility- towards the moral management of Organizational Stockholders. Business Horizons, 34(4), 39–48. doi:10.1016/0007-6813(91)90005-G

- Carroll, A. B. (1998). The four faces of corporate citizenship. Business and Society Review, 100–101(1), 1–7. doi:10.1111/0045-3609.00008

- Carroll, A. B. (1999). Corporate social responsibility. Business and Society, 38(3), 268–295. doi:10.1177/000765039903800303

- Carroll, A. B. (2008). A history of Corporate Social Responsibility, Concepts and Practices. A. M Andrew Crane, D, Matten, Moon, J., & Siegel, D. The Oxford handbook of corporate social responsibility (PP-19-46). New York: Oxford University Press.

- Carroll, A. B. (2015). Corporate Social Responsibility. Organizational Dynamics, 44(2), 87–96. doi:10.1016/j.orgdyn.2015.02.002

- Carroll, A. B., &Shabana, K. N. (2010). The business case of Corporate Social Responsibility, a review of concepts, research and practice-International. Management Review, 12(1), 85–105.

- Certified CSR Professional certification course of ICSI, Study Materials.

- Dona, W. J. (2010). Measuring corporate social performance—A review.International Journal of Management Reviews. doi:10.1111/j.1468-2370-2009.00274.x

- Fisch, C., & Block, J. (2018). Six tips for your systematic literature review in business and management research. Management Review Quarterly, 68(2), 103–106. doi:10.1007/s11301-018-0142-x

- Godfrey, P. C. (2005). The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. Academy of Management Review, 30(4), 777–798. doi:10.5465/AMR.2005.18378878

- Ismail, M. (2009). Corporate Social Responsibility and its role in community development: An international Perspective. Journal of International Social Research, 2(9, fall).

- Jatana R, (2007). Corporate Social Responsibility (Theory and Practice with case studies). Deep and deep publications Pvt Ltd.

- Kalyani, K. (2018), CSR-monitoring from “I” to “we” to create new India, The Management Accountant 53(12)

- Kaushik, V,K (2017), CSR in India: Steering Business toward Social Change, LexisNexis

- Kumar, R, Bapat, S, Singh, R, (2020) Know everything about Corporate Social Responsibility, Xpress Publishing

- Kundu, B. (2014). Corporate social responsibility practices of selected power and electricity companies in India. International Journal of Research in Social Sciences November(2014) (ISSN, 2249–2496).

- Lal. K Niraj, DuttaArchana. (2012), Sharda Trust. An Arvind Limited Initiative to help the Urban Poor. Vikalpa. SAGE Publications, 37(2, April–June);ISSN: 0256-0909(print), 2395-3799(web).

- Lalitha, V., & Melissa, S. (2012). Creating shared value in India: The future for inclusive growth. Print, 37(2), April–June);ISSN: 0256-0909, 2395-3799(web): & Applied Management Research. ISSN: 2349-5677: Volume 1, issue 11, April 2015.

- Lohia, R,(2020) CSR Activities & Projects under the Companies Act 2013 along with SocialAudit, XcessInfostore (P) Ltd.

- Lumde, R(2018), Corporate Social Responsibility in India: A Practitoners Perspective, Notion Press.

- Manfred, B. M., &Zinette, B. (2013). Retrieved from http://www.mdpi.com/journal/sustainability. 2019,11. emacher ,Teschemacher Yael, Arora B, Jyoti D, Sengupta, R,(2019), Corporate Social Responsibility in India: . . Academic Perspectives on the Companies Act, 5939, n10.3390/su11215939.doi:doi

- Moon ,J( 2014) Corporate Social Responsibility, A very Short Introduction, Oxford University Press.

- Nantu, P. R. (2018). Corporate Social Responsibility- A Dynamo Generating Basic Amenities for low lying societies, The Management Accountant,53(12).

- Nidhi, S., &Kundu, B. (2014). A comparative study of corporate social responsibility practices of selected public and private sector companies in India .Periodic Research. 2(4),ISSN NO: 2231-0045, II(IV, May).

- Niharika, V., & Rahul, S. (2012). Corporate social responsibility, practice, theory and challenges.Vikalpa. SAGE Publications, 37(2, April–June);ISSN: 0256-0909(print), 2395-3799(web).

- Paleri, P (2020) Corporate Social Responsibility,Concept, Cases and Trends, Cengage Publishers.

- Pierick, E., Teen, V., Beekman, C. N., Van Derweele, M. J. G., &Meenzen, R. P. M. de Graff. (2014). A Framework for analyzing Corporate Social Performance beyond the Woods Model. The Hague: Agricultural Economics research Institute [Report]. 5.04.03: ISSN 90-5242-923-5

- Priyanka, S.(20160 Corporate Social Responsibility: Its role &challenges in Indian Context: International Journal of Applied Research: 2016,2(3)-294-297.ISSN Print 2394-7500. ISSN online: 2394–5869.

- Retrieved from http://www.csrbox.org.

- Retrieved from http://www.k4d.org/Health/sustainable-development-challenges-and-csr-activities-in-india.

- Sahay, B.S, Das, S, Chatterjee, B, Subhramaniam, G, Rao, R, V, (2016)CSR, The New Paradigm, Bloomsbury

- Sarabu, V. K. (July 2017). Corporate social responsibility in India: An overview. Asian Business and Management, 9, No !, 53–67.

- Srikanth, P. Dr. (2018). CSR Performance and advertisement Expenditure and its impact on revenues of the Companies, The Management Accountant ,53(12).

- Vasanthi, S. (2012). Developing a. Responsible Business Course for Business Schools in India- Vikalpa. SAGE Publications, 37(2, April–June);ISSN: 0256-0909(print), 2395-3799(web).

- Vijayta, D., &Pradyumana, K. (2012). An institutional perspective on corporate social responsibility.Vikalpa. SAGE Publications, 37(2, April–June);ISSN: 0256-0909(print), 2395-3799(web).